We all like to think about retirement as the years when we

can afford to stop working and start traveling, playing golf,

relaxing, or spending more time with our loved ones. While you may be dreaming

about your gold�en years, how much thought have you given the funds that you

will need to make your retirement dreams a reality? The truth is, those who

commit to a disciplined investment strategy today may have a better chance at

achieving the retirement of their dreams.

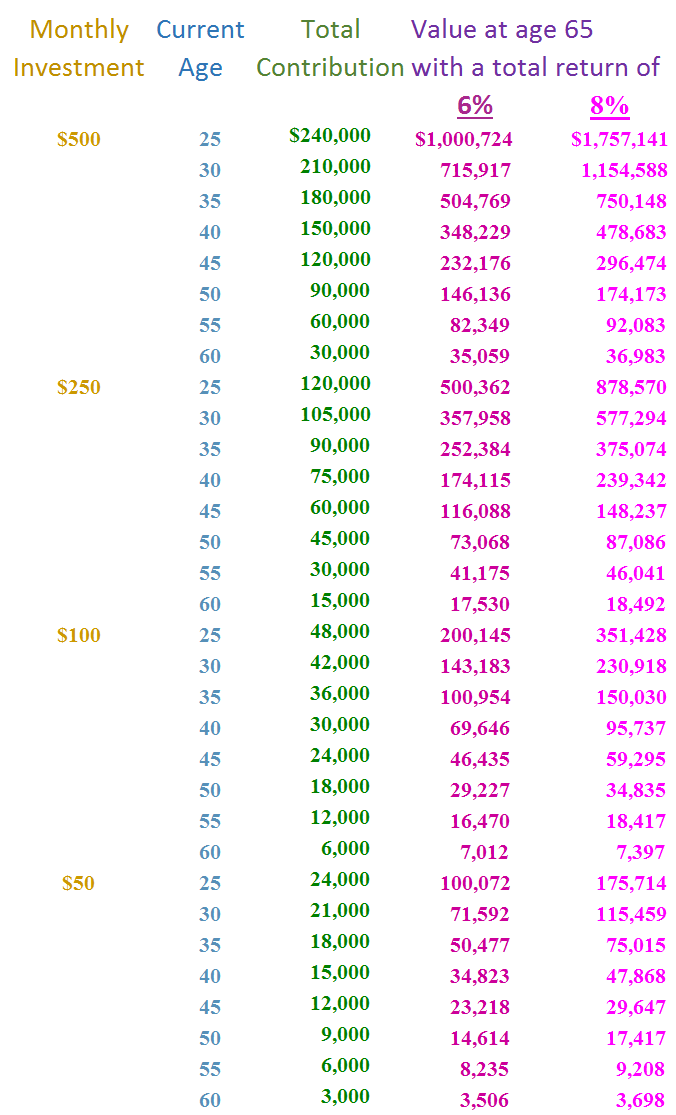

This chart shows the importance of establishing a systematic

investment plan, and how starting an investment

plan at different life stages can accumulate varying amounts upon reaching age

65. The chart shows three, important factors that can influence retirement

funds:

� The Power of Compounding. Compounding,

sim�ply put, is when an investment generates earnings on reinvested earnings.

When this theory is utilized in retirement accounts, where funds may be

accumulated for years or even decades, it can be pretty powerful. The longer

money is left in the account, the faster it begins to grow, which is a clear

indication of the importance of starting a

retirement fund as early as possible.

� Dollar-Cost Averaging. By utilizing a

systematic investing plan, which includes investing on a regular basis,

investors may take advantage of dollar-cost averaging. With dollar-cost

averaging, investors buy more shares when the price of an investment has

declined and fewer shares when the price has risen. Over time, the cost of the overall investment may be lower and investment risk may be reduced by not

investing substantial amounts at the wrong time. Keep in mind that dollar-cost

averaging does not assure a profit or protect against a loss in declining

markets, and before embracing the dollar-cost averaging strategy, investors

should consider their ability to continue investing during periods of falling

prices.

� Choosing the Right Mix.

Investors with a longer invest�ment time horizon may take advantage of more

growth-oriented investments, which

typically offer a higher average return based on their increased risk. By

selecting investments that have the potential to achieve higher than average

returns, investors can possibly increase their potential to accumulate greater

assets for retirement. Of course, every investor needs to carefully evalu�ate

their tolerance for risk, ability to invest, and investment time horizon

before selecting their specific investments.

Planning for a successful

retirement can be the key to helping ensure that your retirement goals become

a reality. For more information on how you can begin to plan for the

retirement of your dreams, contact your Financial Advisor